Productivity growth is about the transformation of products, processes, and workplace practices. In all three of these contexts, business investment plays a central role, whether that be investment in new ideas, in new locations for expansion, or in technology to change workplaces practices and production.

Business investment and productivity growth increase the potential for the economy to deliver higher living standards. Business investment is not the only or the whole story – public investment and enhanced labour participation and skills are also needed (and are addressed in other work programmes). The objective of this research programme is to take a fresh look at UK investment and the role for finance in supporting it.

The lens for distilling and synthesising this new research builds from the three perspectives that were proposed in the framework paper, UK Business Investment: Economists, Managers, Financiers prepared for the first year of the TPI research programme.

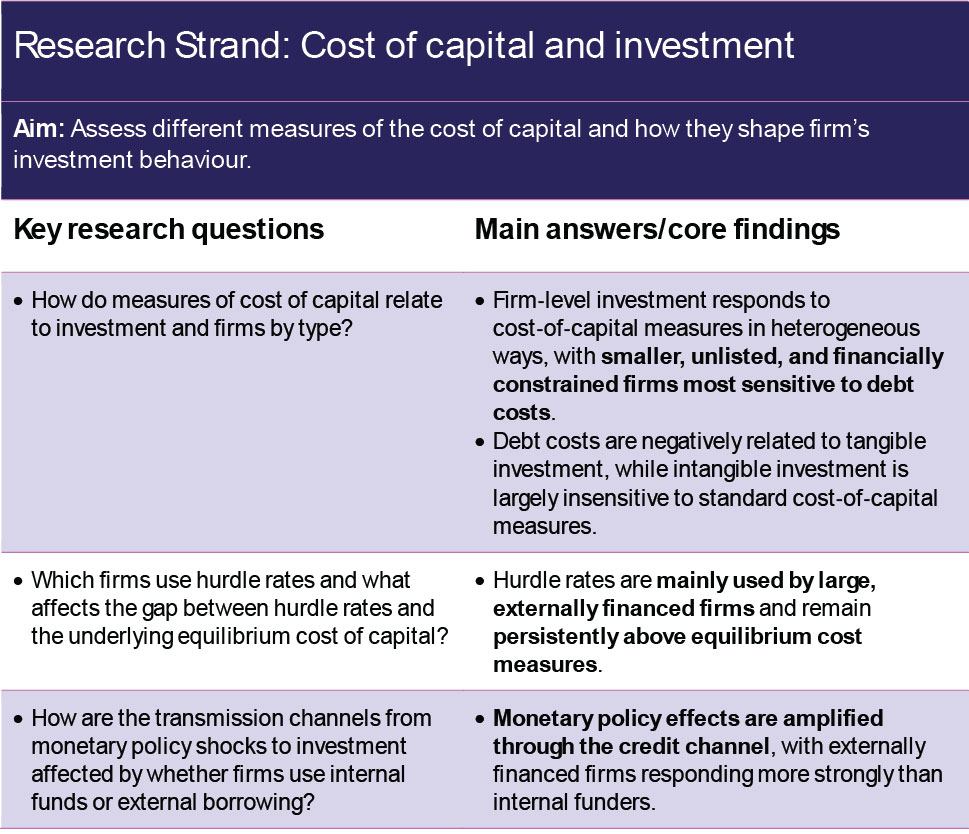

The equilibrium/economist perspective is the canonical perspective where investment is undertaken up to the point where the cost of capital equals its marginal return. However, the cost of capital, and therefore business investment outcomes, vary according to heterogeneity of firms as well as the macro- and micro-economic environment.

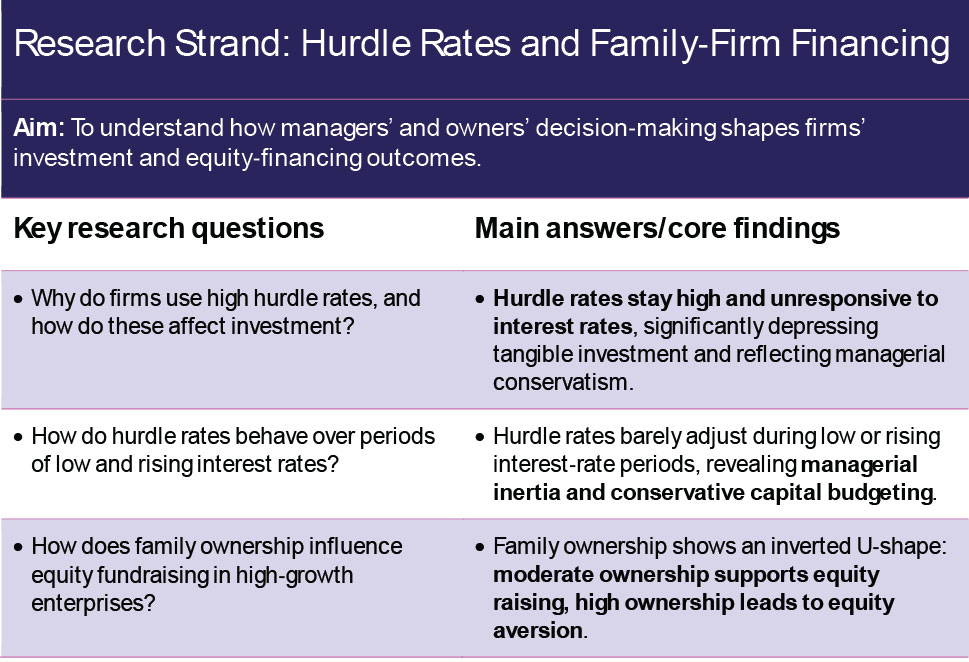

The demand/manager-owner perspective accounts for how firm owners’ objectives can affect the relationship between finance and business investment. Under some circumstances, manager-owners might be the constraint yielding less finance demanded and therefore less investment undertaken than would be suggested by the equilibrium/economist perspective.

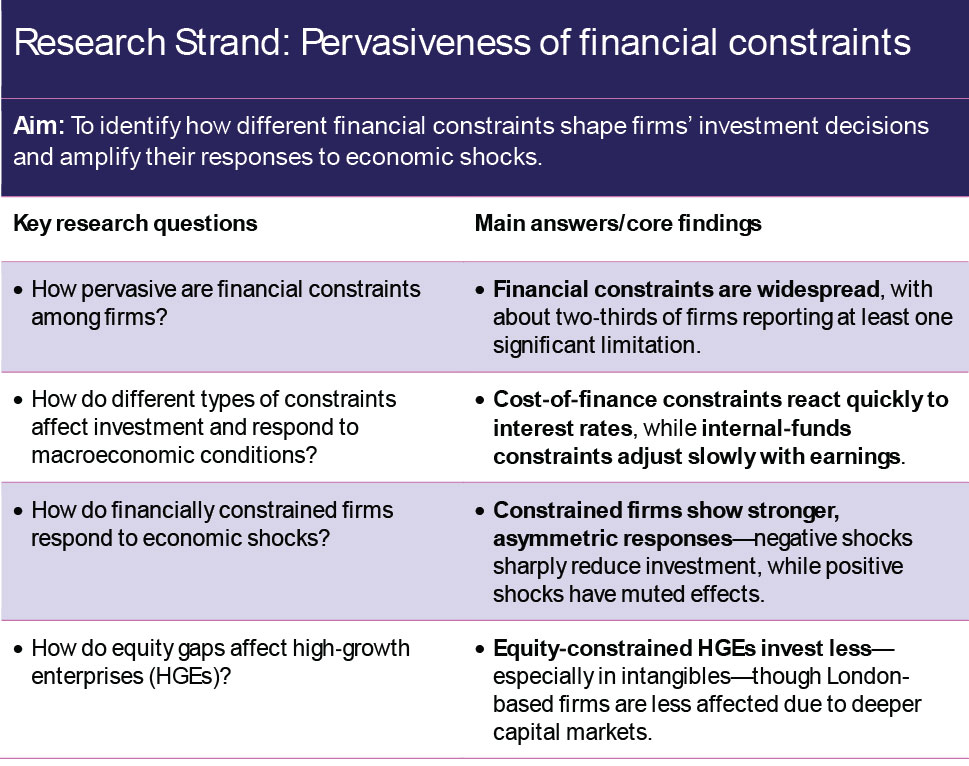

The supply/financier perspective considers the objectives of financial institutions in the finance and investment equation. These considerations may yield less or more costly finance than might be supplied to support investment than would be suggested by the equilibrium/economist perspective.

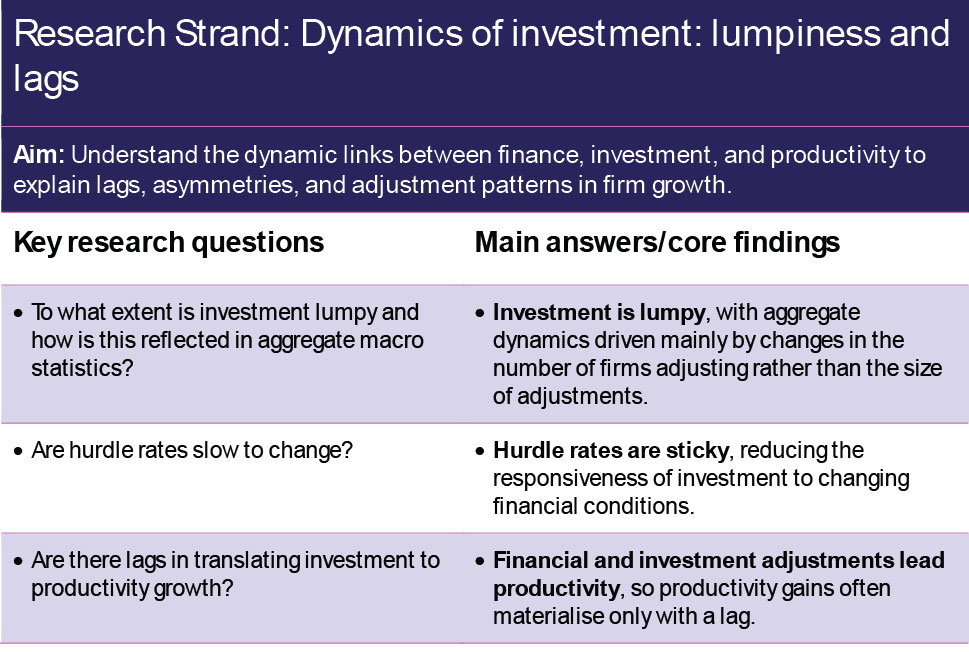

Finally, there is a dynamic perspective which investigates how sticky or slow decision-making and lumpy investment strategies or projects can affect the time-series properties of firm behaviours and outcomes and through those channels the evolution of productivity growth.

Research undertakings in this programme focus on the cost of capital and investment, including an assessment of different measures of the cost of capital (debt, equity, weighted average cost of capital (WACC), hurdle). The work investigates how those are related to investment of different types (tangible vs R&D). How the firm’s balance sheet evolves when investment is lumpy is relevant. The work shows that investment outcomes vary by firms of different employment size, high-growth designation, productivity, financial constraint, region, and with different ownership structures (particularly considering the family owner).

Macroeconomic environments and policy shocks can be relevant for investment outcomes. All the research papers in this programme use firm-level data, including survey, qualitative, and quantitative.

Heterogeneity is the key finding. There is no ‘one-measure fits most’ for the cost of capital in econometric research. The relevant cost of capital varies by firm size, location, family ownership, and type and lumpiness of investment. Further, the gaps between different measures of the cost of capital — for example, the cost of debt vs the hurdle rate – are related to the macro environment and policy. This leads to the observation that investment responsiveness is asymmetrical to the macro environment given firm characteristics.

More broadly there are lags and stickiness between hurdle rates, investment, and productivity. Findings also show that investment responsiveness is non-linear in various firm characteristics. There is a U-shaped relationship between investment and financial constraints, family ownership, and productivity levels.

Author Catherine L. Mann