What explains the UK’s productivity problem?

The UK has experienced significantly slower productivity growth than comparable countries over the decade and a half since the global financial crisis. Three fundamental challenges need to be tackled urgently: underinvestment, inadequate diffusion and an absence of joined-up policy-making. This blog was written by Professor Bart van Ark, Managing Director of The Productivity Institute, and Professor Mary O’Mahony, Research Director of The Productivity Institute, based on insights from their work in The Productivity Agenda report.

The UK faces a tough productivity challenge. Slow productivity growth threatens the much-needed revival of economic growth and improvements in living standards and wellbeing. Slower growth of the population and the workforce make the challenge of improving productivity over the next decade a daunting one. If the current trend in productivity growth continues for the next two decades, it will not be possible to maintain current living standards, let alone deliver sustainability and improved wellbeing.

UK growth

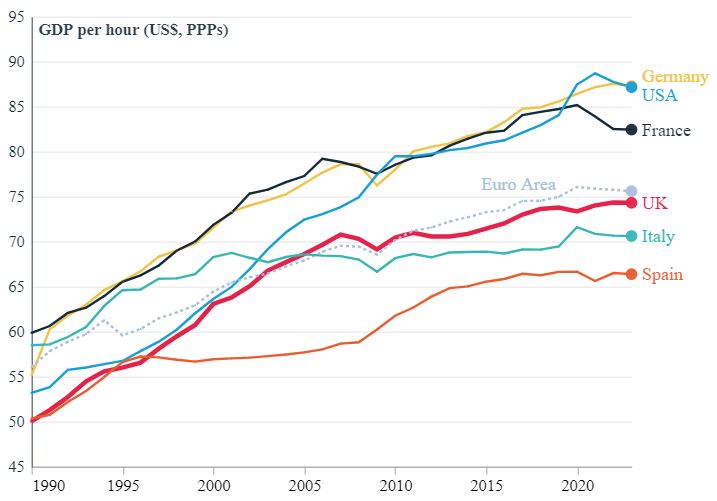

The UK has performed particularly badly relative to comparable economies in terms of productivity growth. It is in the bottom half of the rankings in the OECD, well below France, Germany and the United States; just below the average for the euro area; and slightly ahead of Italy and Spain. From 2010 to 2022, the annual average growth in UK GDP per hour worked was just 0.5%, with little sign of improvement in recent years.

Figure 1: GDP per hour (in US$, PPP converted), 1990-2023

Source: The Conference Board Total Economy Database, April 2023

Low productivity levels seriously affect the resilience of the UK economy, making it more vulnerable to economic shocks, especially at a regional level. Some parts of the country are severely underperforming relative to their own history and compared with equivalent places in other countries.

Many firms at the bottom of the productivity distribution are not resilient or adaptive, and are barely surviving the economic pressures they are currently facing. And many people who are low skilled and (if working at all) employed in relatively unproductive jobs are struggling to get by.

Even doubling the current productivity growth rate – from 0.5% to 1% a year – over the next 12 years will only be sufficient to achieve the same rate of GDP growth as in the past decade. To strengthen improvements in people’s living standards in future, annual productivity growth would therefore have to increase to about 1.5% or more.

The three key challenges

Why the UK has experienced slower productivity growth than elsewhere remains the subject of intense debate. Indeed, the ‘puzzle’ of productivity can be imagined as a complicated 1,000-piece jigsaw.

Nevertheless, research by the Productivity Institute – as documented in our recent publication The Productivity Agenda – points to three fundamental issues that need to be tackled urgently to close the gap relative to the UK’s growth performance before the global financial crisis of 2007-09, and compared with the countries that have performed better since. Those issues are, in essence, underinvestment, inadequate diffusion and an absence of joined-up policy-making.

Chronic and broad-based underinvestment in the UK economy

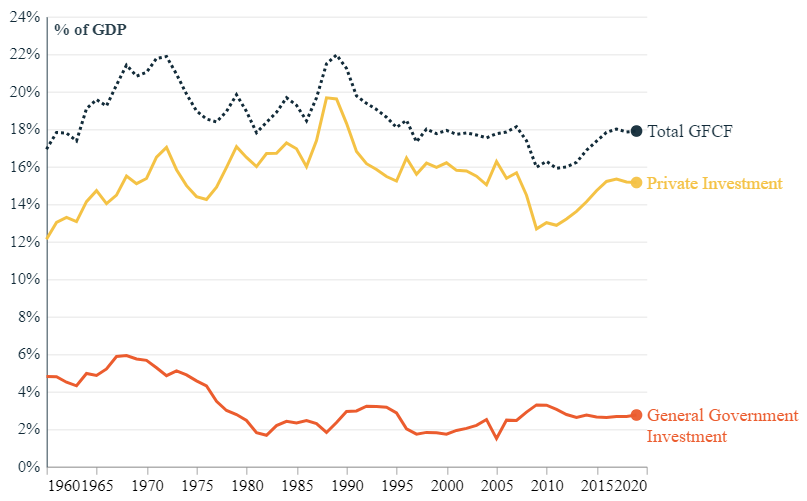

The UK has experienced a slowdown in investment growth in recent decades that is broad-based, including both public and private capital.The weak investment is across industries, but is especially notable in manufacturing, finance and insurance, and business services (Alayande and Coyle, 2023).

Capital investment is also unequally distributed across the UK regions, just like economic activity and employment. There is significant variation both between high- and low-productivity regions of the UK, and also large variation within regions (Becker and Martin, 2023).

Figure 2: Total investment (as a percentage of GDP) split by public and private, 1960-2022

Source: Chadha and Samiri, 2022

Underinvestment is also visible in training and the development of skills – or the creation of human capital. Despite gains in terms of the share of higher educated people in the workforce, the lack of investment has trapped many UK firms in a low-skill, low-wage, low-productivity mode of operation.

This has created a vicious cycle where, once the demand for high-level skills evaporates, so do the incentives to supply such skills through education and training. This helps to explain the declining trend of firms providing training, as they lack incentives to take steps such as developing advanced skills modules via further education colleges and other providers (Grimshaw et al, 2023; Grimshaw and Miozzo, 2021; Green et al, 2020; Nelles et al, 2022).

The growth of capital deepening in intangible capital, including assets like research and development (R&D) and software, as well as marketing, branding and organisational capital, has held up better than that for tangible assets such as equipment and structures. This has not yet been translated into a recovery in productivity across the whole economy – or total factor productivity growth – suggesting a lack of spillovers from those investments (van Ark et al, 2023).

Finally, although underinvestment is chronic and has been ingrained in the UK’s economic system for decades (Chadha and Venables, 2023), there is evidence that the austerity measures in place from 2010 have particularly contributed to weakened public investment (Resolution Foundation, 2023). Emerging evidence also indicates that Brexit has had a negative impact on private investment (Haskel and Martin, 2023).

Inadequate diffusion of productivity-enhancing practices between firms and places

The UK is very active at the frontier of science and knowledge creation. It is regarded as one of the most innovative nations, ranking fourth in the 2023 edition of the Global Innovation Index.

Yet its presence in its main areas of specialisation – notably artificial intelligence, quantum technology and synthetic biology – is rather narrow and involves relatively few companies (Nightingale and Philips, 2023).

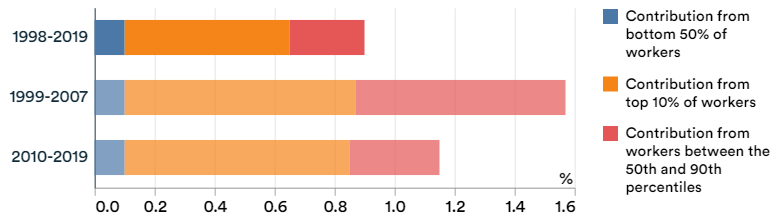

Nevertheless, the productivity growth contribution from UK firms for the non-financial business economy in the top decile of the distribution of firms’ (level of) productivity is very strong, according to firm-level data from the Office for National Statistics (ONS). It has not shown any sign of dropping off and is now contributing the bulk of current productivity growth.

In contrast, firms with above-median productivity levels (in the sixth to ninth decile of the distribution) have accounted for the lion’s share of the productivity slowdown in the non-financial business economy since the global financial crisis.

These firms, which have the potential to be productive, have not benefited from the diffusion of technology and innovation from the most productive companies. This has been exacerbated by stagnant foreign trade, changing patterns in foreign direct investment (Driffield et al, 2023) and the UK’s lack of deeper integration in global supply chains.

Figure 3: Contribution of firms with different worker productivity levels to change in average productivity growth, non-financial business economy, 1998-2019, percentage

Source : ONS, 2023

Institutional fragmentation and lack of joined-up policies

The UK is characterised by a dichotomy in policies and institutions that affect productivity. On the one hand, many pro-productivity policies are highly centralised, including education, innovation, transport, planning and regional development.

On the other hand, the institutional landscape of productivity-supporting institutions is highly fragmented in terms of function and location, ranging from local and combined authorities to the governments of the devolved nations. It also includes city deals, town funds, local enterprise partnerships and local skills improvement plans (Coyle and Muhtar, 2023; Westwood et al, 2021; McCann, 2021).

In other countries, ‘mid-level’ governments typically have substantial devolved responsibilities for policies with a big impact on productivity. This is particularly the case with infrastructure and planning, which are characterised by large externalities – costs or benefits to third parties.

There are persistent and relatively large gaps in regional productivity in the UK. Major second-tier cities such as Birmingham, Glasgow and Manchester still show large productivity gaps. The gaps are not only relative to London: these cities also have productivity levels well below those of comparable cities in continental Europe.

Examples of turnaround cities that have faced similar challenges from post-war deindustrialisation suggest that the journey has been made more difficult in the UK because of a lack of devolved government, coordinated policy-making and sustained funding (Frick et al, 2023).

This means that in the UK it is difficult for any national government policy to be translated into effective local policy. At the same time, local governments are under-resourced and lack the authority to develop and implement a place-specific and integrated investment strategy.

Productivity for inclusive growth

How can the UK accelerate investment, including in skills and intangibles, across a wide range of industries and across the country? How can the diffusion of productivity-enhancing practices between firms, places and people be strengthened? And how can the UK overcome its fragmented policy and institutional landscape at all levels?

The Productivity Agenda describes the need for an integrated approach to pro-productivity policies to improve the performance of people, firms and places. The government needs to commit to a productivity agenda for the long term to provide direction and stability. It also needs to co-ordinate with businesses and public sector organisations, and with workers, in implementing and executing productivity-enhancing practices.

Improving productivity would benefit all of the UK’s people and firms, wherever they are located. If growth is not inclusive, with the ultimate goals of wellbeing and sustainability at its core, the UK’s ambition of raising productivity will fail.

There are three key elements to enabling productivity-supporting inclusive growth. First, it is important that as many people, firms and places get access to the resources and opportunities to improve productivity.

Second, all resources for productivity growth are scarce, and it is therefore critical to use them efficiently and effectively to create better outcomes. This is at the core of our productivity agenda.

Finally, the gains from productivity growth need to be distributed widely. Firms and investors but also people and places need to benefit and see the rewards reinvested in a way that will support higher living standards and wellbeing. This will also make places more attractive in terms of where to live, work and do business.

This blog was first published by Economics Observatory where a list of further reading and experts can also be found.